By now, you might have heard about legislation from the EU which will mean more sustainability reporting – the CSRD, or Corporate Sustainability Reporting Directive.

What is it and why have they introduced it?

The CSRD was introduced last year to EU member states. Companies must reporting on social and environmental information. This has broadened the host of companies who have previously had to report, to include more large companies as well as some SMEs.

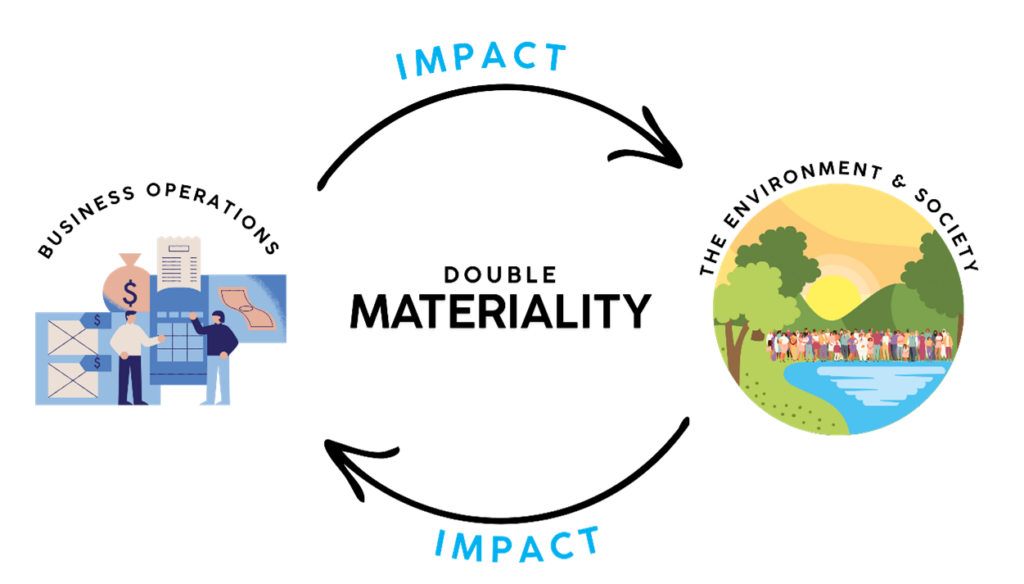

The reasoning for the EU bringing in this legislation is to make sure that investors (and other stakeholders) can access this information easily, and can make informed decisions on:

- The risks to people and the environment posed BY the company

- The risks to the COMPANY posed by the environment and other sustainability issues.

This new reporting framework brings in a concept which companies would benefit from assessing, whether they have to report or not – double materiality.

As a business, your operations will impact the environment and society, positively or negatively. For example, if you are a large multinational company, employing thousands of people, the labour standards for your workers (good or bad) will have an impact on society.

In reverse, changes in the environment, such as climate change, might affect your business operations. Increased flooding, for example, might disrupt logistics for deliveries or put infrastructural assets at risk of damage. This is the impact the environment has on you.

Regardless of whether you legally need to report these impacts or not, this impact assessment is an exercise each business should be completing as a responsible part of society.

How does your event carbon footprint fit into this?

Currently, in the UK, SECR reporting undertaken by larger companies is only mandatory across Scopes 1 and 2. Under CSRD, Scope 3 will now need to be reported on. Scope 3 includes your suppliers up and down the value chain, including the activities undertaken by event suppliers. These might include (but aren’t limited to):

- The venue you have chosen

- Your caterers

- Transport companies

- Exhibition and signage suppliers

The activities of these suppliers will create Scope 3 carbon emissions. To be able to report your Scope 3 emissions, you need to know what they are. Carbon Consultancy and Carbon Disclosure use DEFRA GHG Emissions Factors and present the carbon footprint based on the UK Government’s reporting requirements for Scope 3. You can therefore be confident that your event carbon emissions data is compliant, if you need to report it.

Is this applicable to my company?

Firstly, it’s important to note that your Finance and/or Legal departments should be able to tell you if this will be a legal requirement. It all depends on your legal structure, size and operations in the EU. However, regardless of your size or location of your headquarters, if you have significant activity in the EU, you will most likely need to begin reporting under CSRD in the next few years. For a more in-depth guide to when this might be applicable between 2025 and 2029, take a look at this summary from Sabrina Freitas at Deloitte.

Meet your legal reporting requirements with Carbon Consultancy

Book a free introduction call with one of our sustainability specialists to understand your reporting obligations and what will be required under this new legislation. Call 02476 369 720.